What's Going on in the Markets September 9 2016

On Friday September 9 2016, the S&P 500 index fell 2.4%, while the Dow Jones Industrial Average fell 2.1%. This was the first "greater than 1%" sell-off since June, its worst single-session loss in more than two months. The drop ended a relatively quiet summer for U.S. stocks, which had touched new highs in mid-August. But despite Friday's jarring downdraft, market internals remain solid and equity markets are within stones throw of their recent peaks. Of course, the press reports are describing it as a full-blown market panic.

Even if the short-term pullback in stocks persists, we do not believe the longer-term bull market—which has been underway since 2009—is dead. U.S. economic data has generally shown signs of strength, and an improving economy should support the stock market over the long term.

So what’s going on? Efforts to trace the reason why quick-twitch traders scattered for the hills on Friday turned up two suspects. The first was Boston Federal Reserve President Eric Rosengren, who sits at the table of Fed policy makers who decide when (and how much) to raise the Federal Funds rate. On Friday, he announced that there was a “reasonable case” for raising interest rates in the U.S. economy. According to a number of observers, traders had previously believed there was a 12% chance of a September rate hike by the Fed; now, they think there’s a 24% chance that the rates will go up after the Fed’s September 21-22 meeting. Oh the horror of a less than 1 in 4 chance of a quarter-point (0.25%) rise in short-term interest rates--sell everything!

If the Fed decides the economy is healthy enough to sustain another rise in interest rates—from rates that are still at historic lows—why would that be bad for stocks? Any rise in bond rates would make bond investments more attractive compared with stocks, and therefore might entice some investors to sell stocks and buy bonds. However, with dividends from the S&P 500 stocks averaging 2.09%, compared with a 1.67% yield from 10-year Treasury bonds, this might not be a money-making trade.

If the possibility of a 0.25% rise in short-term interest rates doesn’t send you into a panic, maybe a pronouncement by bond guru Jeffrey Gundlach, of DoubleLine Capital Management, will make you quiver. Gundlach’s exact words, which are said to have helped send Friday’s markets into a tailspin, were: “Interest rates have bottomed. They may not rise in the near term as I’ve talked about for years. But I think it’s the beginning of something, and you’re supposed to be defensive.” My thoughts on this: pundits have been declaring the end of the bull market in bonds for many years and have been proven wrong time and time again. Statements like this are pretty worthless in my opinion. Could he be right? Sure, there's a 50/50 chance.

Short-term traders appear to have decided that Gundlach was telling them to retreat to the sidelines, and some have speculated that a small exodus caused automatic program trading—that is, money management algorithms that are programmed to sell stocks whenever they sense that there are others selling. After the computers had taken the market down by 1%, human investors noticed and began selling as well.

Uncertainty about central bank policy outside the U.S. was another potential cause for Friday’s volatility. On Thursday, the European Central Bank opted for no new easing moves and Japanese bond yields have continued to rise. The two events have sent a message to markets that quantitative easing (bond buying and other monetary stimulus) may have lost some of its efficacy and will not continue indefinitely.

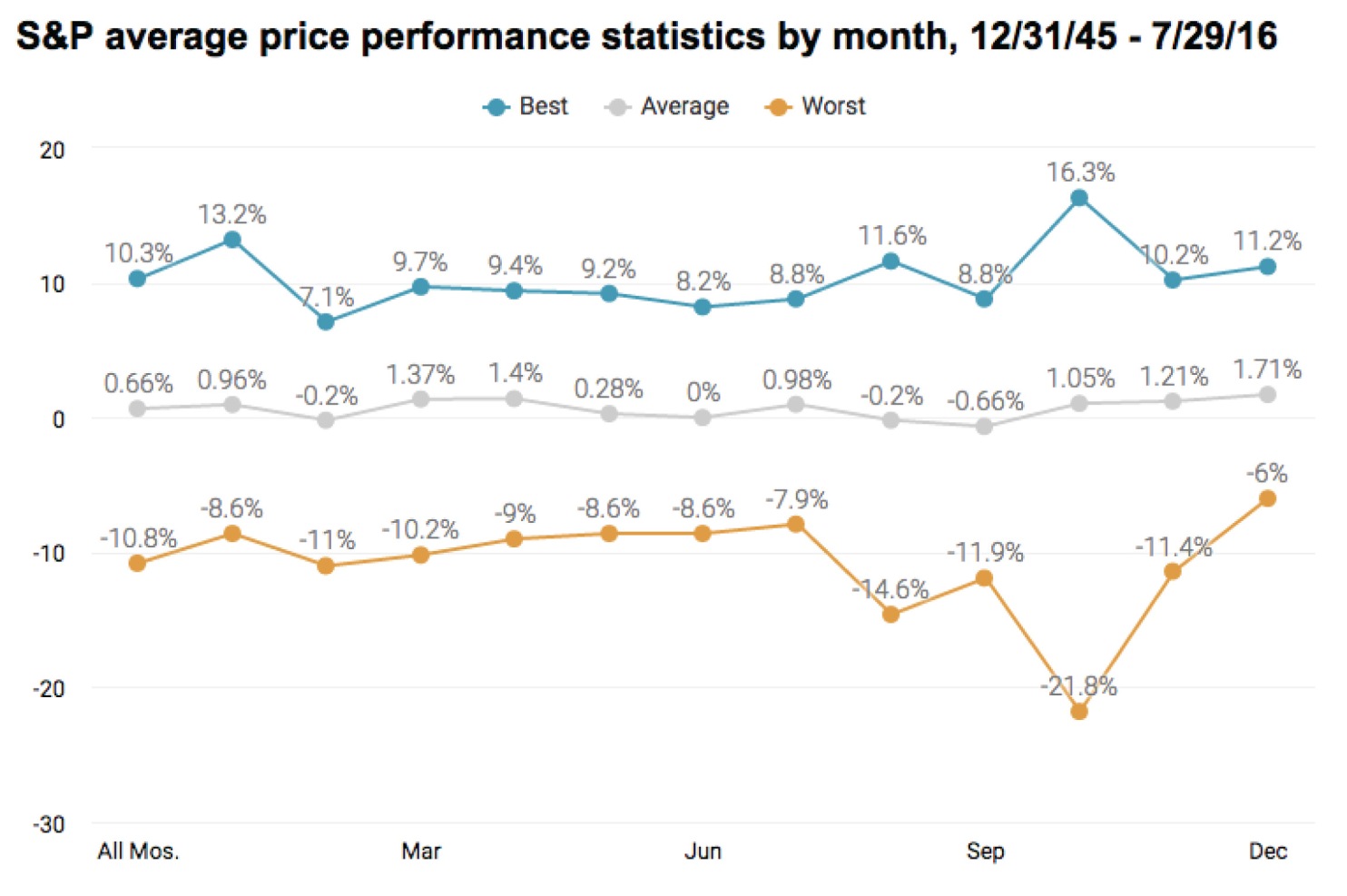

For seasoned investors, a 2% drop after a very long market calm simply means a return to normal volatility. This is generally good news for investors, because volatility has historically provided more upside than downside, and because these occasional downdrafts provide a chance to add to your stock holdings at bargain prices. I've been telling clients all summer long to expect a volatile and rocky September and October. Does that make me smart? Nope, historically, periods of calm like we've seen are always followed by volatility. September and October tend to be more volatile than other months of the year. Markets have been unusually calm this summer, and prolonged periods of low volatility can make markets susceptible to news and rumors. Given the emphasis the market is now placing on Fed policy—and the uncertainty surrounding it—we wouldn’t be surprised to see markets continue to experience volatile swings when news or economic data suggest the Fed may, or may not, raise interest rates.

That doesn’t, of course, mean that we know what will happen when the exchanges open back up on Monday, or whether the trend will be up or down next week or for the remainder of the month. Nor do we know whether the Fed will raise rates in late September, or how THAT will affect the market.

As for bonds, while rising interest rates can translate into falling bond prices—bond yields typically move inversely to bond prices—it’s important to remember that yields generally don’t move in tandem all along the yield curve. The Fed influences short-term interest rates, but long-term interest rates are generally affected by other factors, such as economic growth and inflation expectations. And even if the Fed does raise short-term interest rates again this year, I would anticipate that future rate hikes would be gradual, as inflation remains low and the U.S. economy is only growing moderately.

That said, periods of market volatility are a good time to review your risk tolerance and make sure your portfolio is aligned with your time horizon and investing goals. A well-diversified portfolio, with a mix of stocks, bonds and cash allocated appropriately based on your goals and risk tolerance, can help you weather periods of market turbulence.

All we can say with certainty is that there have been quite a number of temporary panics during the bull market that started in March 2009, and selling out at any of them would have been a mistake. You must resist overreacting to swings in the market. Stock market fluctuations are a normal part of investing; panicking and pulling money out of the market may mean missing out on a potential rebound.

The U.S. economy is showing no sign of collapse, job creation is stable and a rise in interest rates from near-negative levels would probably be good for long-term economic growth. The Institute for Supply Management survey for the manufacturing sector recently showed an unexpected decline, and the service sector moved down by more than economists had expected, so I will be monitoring upcoming survey results closely to see if this develops into a trend. The employment situation remains firm; new job openings hit a record high in July and new claims for unemployment remain near recent lows.

While it may be prudent to trim some profits, panic is seldom a good recipe for making money in the markets, and our best guess is that Friday will prove to have been no exception. Market volatility is unnerving, but it’s a normal—and normally short-lived—part of investing. If you’ve built a solid financial plan and a well-diversified portfolio, it’s best to ignore the noise and focus on your long-term goals.

If you would like to review your current investment portfolio or discuss any other financial planning matters, please don’t hesitate to contact us or visit our website at http://www.ydfs.com. We are a fee-only fiduciary financial planning firm that always puts your interests first. If you are not a client yet, an initial consultation is complimentary and there is never any pressure or hidden sales pitch. We start with a specific assessment of your personal situation. There is no rush and no cookie-cutter approach. Each client is different, and so is your financial plan and investment objectives.

Sources:

http://thereformedbroker.com/2016/09/09/dow-decline-signals-end-of-western-civilization/?utm

The MoneyGeek thanks guest writer Bob Veres for his contribution to this post

YDream Financial Services, Inc

YDream Financial Services, Inc