What’s Going on in the Markets August 6, 2024

With the lazy, hazy days of summer come the doldrums in the stock markets—or so everyone thought.

July went out with a bang as the market rally broadened significantly to include small-caps and mid-caps, while the red-hot technology stocks took a breather. Sure, the S&P 500 index was only up 1%, but the small caps were up 11%, the mid-caps were up 7%, and even the bonds were up 3%.

But since then, if July was the lion, August has been the bear. The S&P 500 index is down 5% in just three August trading days, the small caps have given back almost 10%, and the tech-heavy NASDAQ 100 has slid 7.5%. In the digital age, markets move fast.

Now, mind you, the S&P 500 is still up about 15% over the last 12 months (and up 9.5% year-to-date), but every 10-12 months, we should expect a 5%- 9% pullback in the markets. We had a 5.3% pullback in April, but the last time we saw a pullback of this size ended last October. The markets have been remarkably calm over the past year, and we went 356 trading days without a 2% daily pullback in the S&P 500 index. That may be why this pullback feels so jarring.

Pundits and the media will posit several reasons for the pullback, such as:

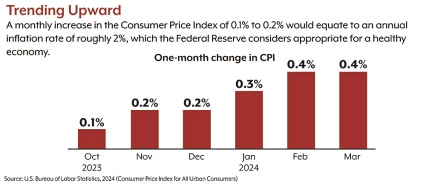

· The Federal Reserve is on the cusp of making a policy mistake by keeping interest rates higher for longer and is pushing the country into a recession.

· The July monthly jobs report, which was out on Friday, spooked traders and investors as it came in much lighter than expected, and the unemployment rate ticked up. This fanned the fears that a recession was on the way (there’s always a recession on the way; the trick is knowing when we’re in one.)

· Over the weekend, news broke that legendary investor Warren Buffet sold half of his stake in Apple during the past quarter and is stockpiling cash.

· The possibility of a bigger, more freely spending government—regardless of party—is giving traders fits. The markets crave certainty, and summertime offers little of it in election years.

· Escalating tensions in the Middle East.

· The unwinding of a long-running Japanese Yen carry trade, in which traders sold the Yen and invested it in higher-paying countries and other opportunities for months if not years. Now, that trade is unwinding and directly affects the world’s stock markets.

You can cite any of the above reasons for the selloff, but the selling will stop when the fear that’s getting the better of so many traders and investors goes away. But certainty about the election is about three months away. Absent a market crash, any possibility of a short-term interest rate cut is about 45 days away. So, buckle up, meanwhile.

In our client portfolios, we’ve been getting defensive by taking some money off the table for weeks now. We are hedged with money market cash earning 5%, Treasury Bills, bonds, inverse funds, and options sold against our positions. We’re prepared to get more defensive if things get worse, but this is a time to look for quality stocks and funds that were too expensive about a week ago. We did some shopping for some clients last week.

We’ve had a fantastic start to the year, and historically, an election year tends to be volatile from the summer into September/October. Once the overhang from the election uncertainty is gone, the market should resume its uptrend by the end of the year.

In short, as I’ve repeated before, the secret to success in accumulating wealth is not to get scared out of your positions. It’s never about completely avoiding risk in the markets but reducing risk. If you’re losing sleep over your investments, consider reducing your exposure or contact us to help determine if you’re overly invested.

Meanwhile, try and stay cool!

If you would like to review your current investment portfolio or discuss any other retirement, tax, or financial planning matters, please don’t hesitate to contact us at 734-447-5305 or visit our website at http://www.ydfs.com. We are a fee-only fiduciary financial planning firm that always puts your interests first. If you are not a client, an initial consultation is complimentary, and there is never any pressure or hidden sales pitch. We start with a specific assessment of your personal situation. There is no rush and no cookie-cutter approach. Each client and your financial plan and investment objectives are different.

YDream Financial Services, Inc

YDream Financial Services, Inc